We’re still waiting for a bullish report to come out of the USDA. It didn’t happen in the January 12th series of reports, but no one really expected any bullish numbers. The January 12 reports did contain several important numbers, including:

- “Final” 2017 corn, soybean and sunflower yield and production estimates. The corn yield was increased to a new all-time record of 176.6 bu/ac. The soybean yield was actually lowered from 49.5 bu/ac in December to 49.1 bu/ac in January. The sunflower yield estimate came in at the third highest ever, an incredible yield considering the early season drought across the Dakotas and eastern Montana. It also reflects the quick and dramatic shift in the weather from late July into August and September when temps cooled and rain fell.

- Revised supply and demand estimates were released. Corn ending supplies were increased an insignificant 40 million bushels. Soybean ending supplies were also increased because of a 65-million-bushel reduction in the export forecast. The increase in soybean ending supplies was not quite as big as expected. The USDA doesn’t release a sunflower supply and demand because of the relatively small size of the crop and the limited number of market participants. Wheat ending supplies were also increased.

- The USDA released their first estimate of winter wheat plantings. This plantings report is where the January surprise came. Virtually everybody expected to see a one- to two-million-acre reduction in winter wheat acres, almost all in the hard red winter wheat region. Those expectations were based on two consecutive low protein (and low price) crops plus a dry fall planting season. The USDA showed increased winter wheat acres in Kansas. That sent wheat prices tumbling one more time.

- The quarterly stocks numbers were also released. There were no unexpected surprises in the stocks numbers.

The next important USDA reports will be the planting intentions numbers on March 30. This will be the USDA’s first guess at what farmers will plant in 2018. Today, the market is anticipating less corn, more soybeans and more spring wheat. That will depend on relative crop prices and spring weather.

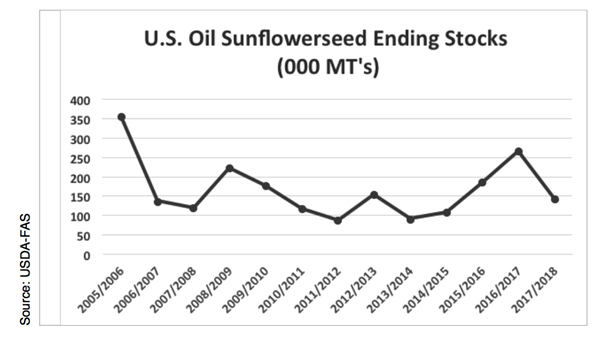

Total production of oil sunflower did drop 22% from last year — mostly the result of a 14% decline in acres. While the USDA doesn’t officially release a sunflower supply/demand report, the Foreign Agricultural Service (FAS) does include sunflower in their data base. The chart below shows their estimate of where U.S. oil sunflower ending supplies will be.

The end result of all of the January USDA report numbers is that we still can’t find a bullish trigger in any of the major markets. Factors that could have a positive impact on prices would be: a substantial increase in export demand for U.S. wheat, corn and soybeans, and any potential weather problems during the last half of the growing season in Brazil and Argentina.

The value of the dollar has declined about 10% in the last year. This is at least somewhat helpful from a price competitive standpoint. We also note that the major investment groups have turned bullish on commodities other than agricultural commodities. Crude oil has traded back above $64 a barrel, the highest in three years. Copper has staged a strong rally. Perhaps some of that commodity enthusiasm will spill over into ag commodities.

Most of the major U.S. wheat producing regions remain very dry. Only the Pacific Northwest and the eastern Corn Belt (soft red winter wheat region) are in good shape from a moisture standpoint.

The Southern Plains experienced some extremely low temperatures on several consecutive nights in late December. It was well below zero across a wide area of Kansas. Temperatures dropped to zero or just above well into Texas. The possibility of winter kill exists, but estimates of the degree of damage vary greatly. We won’t know until the crop breaks dormancy.

Weather and crop conditions across most of Brazil have been very good. Southern Brazil and Argentina, however, have been experiencing a La Niña summer with well below normal moisture. Corn and soybean production will be adversely impacted if this pattern persists.

* Mike Krueger is founder of The Money Farm, a Fargo, N.D.-based grain marketing consulting firm. While the information in this article is believed to be reliable, marketing involves risk, and the author and The Sunflower assume no responsibility for its use.