December, as we expected, was a non-event in terms of market action. The December USDA reports really didn’t change anything. There were no production updates for U.S. crops. The corn, soybean and sunflower yield and production updates will happen in the January USDA reports.

Weather across much of Brazil has been good. However, it has been a slightly different story across southern Brazil and much of Argentina, where hot and dry weather hampered seeding efforts. These dry areas were getting some small relief with scattered rains the last two weeks of December.

The weather outlook across South America was perceived by the market as good in most of Brazil and improving across southern Brazil and Argentina as 2017 drew to a close. That weather outlook pressured the soybean complex back to the low end of recent trading ranges. It was somewhat notable that the large speculative trading funds that had been long soybean and soybean meal futures for many months were actually getting out of those long positions the last half of December. Part of this action was simply the result of year-end position squaring. Part of it was also caused by a mostly non-threatening weather forecast.

The La Niña weather pattern, as discussed last month, is still in place. There is still plenty of time for weather to play a role in these markets over the next two to three months. Soybean planting has gotten late across much of Argentina and part of southern Brazil. That means most of the growing season is still ahead.

Markets should remain rather dull for another couple of months unless there is a weather-related production problem in Brazil or Argentina. There are a few other factors that could change this outlook:

- There could be a bullish surprise in the January USDA reports that no one foresees today. That would almost have to come from smaller quarterly stocks estimates than expected. We don’t see any significant corn or soybean yield adjustments. It’s likely the sunflower yield and production estimates will be increased based on actual harvest results.

- The winter wheat planting estimate should show another significant reduction in planted acres. Cotton will replace hard red winter wheat acres. In addition to fewer winter wheat acres, the Southern Plains remain very dry.

- A sharp increase in export demand, especially for wheat and corn, could also stimulate some buying action in the futures markets. The USDA reduced the wheat and soybean export forecasts in December. They will likely reduce the corn export forecast unless the sales pace starts to accelerate. We do note that U.S. export prices for wheat, corn and soybeans have become competitive with competing markets. We now need to see that translate into actual export sales.

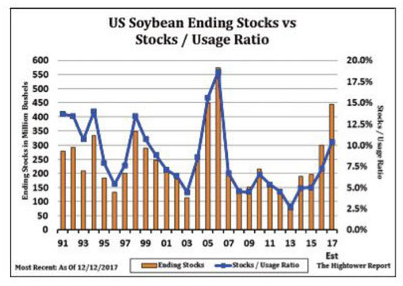

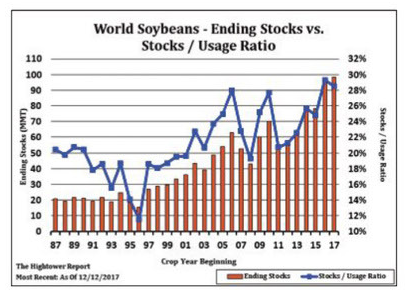

We will likely see more pressure on markets as we head into the spring season across the Northern Hemisphere if none of these potentially bullish factors actually develop. The two charts at below-left show the U.S. and world soybean stocks-to-use ratios. Demand for oilseeds, led by soybeans, has been booming, but so has production.

These stocks-to-use ratios can change quickly in this era of rapidly expanding demand; but record yields for virtually every oilseed in consecutive years has overshadowed the incredible growth in world soybean consumption during the past decade and a half — consumption that went from about 170 million metric tons in 2000/01 to nearly 350 million metric tons forecast for 2017/18.

Long-term views on commodities in general are starting to improve. Some of the major investment houses are touting 10% gains in industrial commodities (crude oil, copper, etc.) in 2018. That optimism is based on a number of factors, including:

- Stronger U.S. and world economic growth than expected.

- Rising interest rates.

- Chatter about inflation.

- Generally low or “cheap” commodity prices.

- Odds money will eventually flow out of equity markets into commodity markets.

Agricultural markets have not been included in these “positive” commodity market forecasts, but they will also benefit from the same factors that will drive gains in industrial commodity markets.

* Mike Krueger is founder of The Money Farm, a Fargo, N.D.-based grain marketing consulting firm. While the information in this article is believed to be reliable, marketing involves risk, and the author and The Sunflower assume no responsibility for its use.